An Open Letter to Ray Dalio re: Bitcoin (Part 3)

An Open Letter to Ray Dalio re: Bitcoin (Part 3)

An open letter to hedge fund colossus Ray Dalio regarding his worldview, the forces of financial nature, and how Bitcoin is bound to reshape both.

Part 2 finished with a look at the pinnacle of Ray’s principled worldview—the idea meritocracy. In Part 3, we dissect the three formulaic elements of the idea meritocracy—radical truth, radical transparency, and believability-weighted decision making—to compare them with the formulation free markets.

Radical Truth

(p.135) “Truth — or, more precisely, an accurate understanding of reality — is the essential foundation for any good outcome.”

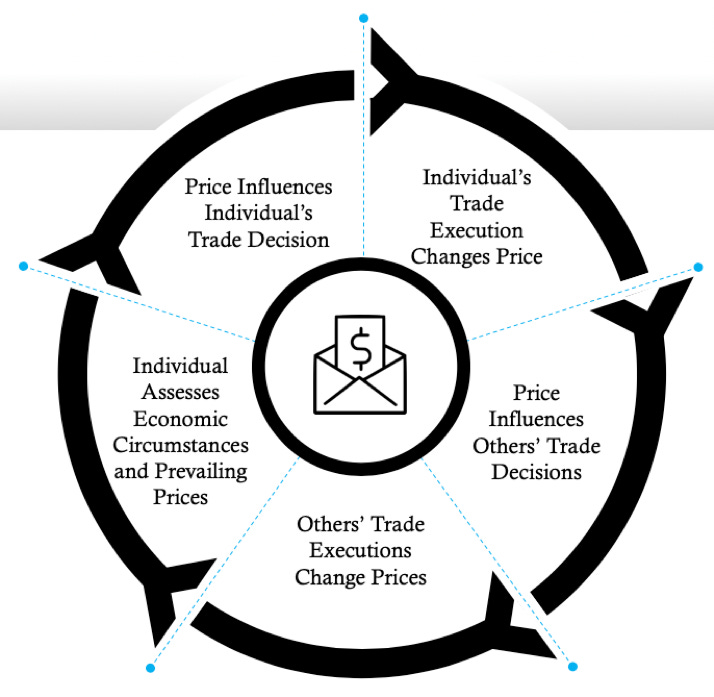

The first element of Ray’s idea meritocracy is Radical Truth, the idea that gaining a clear perception of reality is paramount to facing it head on and dealing with it. In markets, its commonly said that “price is truth”; meaning that all known market realities are expressed in, and evaluated by, any particular asset’s price at any given moment. You may remember from Economics 101 that the market price is the intersection of supply (an objective quality) and demand (an intersubjective or opinion-based quality). Put another way, prices are data packets that convey information about scarcity (which is objective) and value (which is intersubjective). Each entrepreneur’s decision to buy or sell is influenced by prevailing prices and, in turn, communicates back into the market the state of economic conditions relevant to him which, in turn, influences the same decision-making of all other entrepreneurs within his market; this is intersubjective value. These decisions are based on actual availability of time, resources, and know-how; this is objective scarcity. This feedback loop is the means by which free markets dynamically adapt to express prices that accurately portray economic realities:

Let’s return to Larry the lemon farmer: say a storm wipes out a large crop of lemons in California; reduced supply levels of lemons intersecting with an unchanged level of consumer demand necessarily means an increase in lemon prices. Increased prices incentivize lemon growers like Larry to produce more as they now fetch higher prices in the marketplace. On the other side of the lemon market, higher prices disincentivize consumers from buying as many of the sour yellow citrus fruit. As people respond to these ever-shifting incentives, which are a reflection of the endlessly shifting economic realities of supply and demand, free markets adapt to maximize output and minimize costs. In this way, price signals serve as a dynamic incentive system for equalizing supply and demand discrepancies in free markets. However, to maintain truthfulness, these price signals must be freely expressed in a money that is undistorted by government interventionism.

A price signal converts countless economic complexities into simplicity; it compresses myriad market realities down into a single, actionable variable — the market price.

Accurate price signals only prevail if the market is freely competitive and not subject to government interventions such as price fixing, trade restriction, or legal monopoly insulation. In true free market capitalism, most markets are relatively unobstructed by such artifices and the price signals are, accordingly, mostly reliable conveyors of truth. Lemon prices, for instance, tend to reflect the actual underlying supply and demand (or scarcity and value) realities at any given point in time. The market for money, however, is quite different in the modern economy, and its differences have cascading effects across all other markets.

Money is economic water; in the same way water intermixes and intersperses organic chemicals throughout the circle of life, money mediates the interchange of goods, services, and knowledge within markets.

Money, as one half of virtually every economic exchange, is the largest market in the world. This market is monopolized by central banks in every major economy worldwide; meaning that all forms of money competitive to fiat currency are prohibited (see eGold). As Ray aptly points out, (p.533) “Fiefdoms are counterproductive and contrary to the values of an idea meritocracy.” Yet, for some reason, the economic fiefdoms called nation-states, which are antithetical to the free market paradigm (and, therefore, the idea-meritocratic paradigm), are commonplace. Even in the US, where we pride ourselves on being free market capitalists, we maintain this socialistic market structure for money. In this market, the following elements impact price expression of money:

· Supply — the amount of money available to be loaned out (aka loanable funds)

· Demand — the amount of loanable funds desired for borrowing

· Interest Rate — the price paid for funds borrowed

Central banks “manage” the market for money by controlling the supply of loanable funds and setting the interest rate (the price) at which these funds can be lent out. These central bank privileges are preserved by state-enforced monopoly rights, which insulate their mass-produced fiat currencies from competition and eliminate their “skin in the game”. Skin in the game, a crucial Talebian concept, is a property based on symmetry, a balance of incentives and disincentives: in addition to upside exposure, people must also be penalized if something for which they are responsible for goes wrong or hurts others. Skin in the game is a central pillar for properly functioning systems, of both the organic and inorganic variety, and is at the heart of hard money. For gold, its mining costs and risks form the disincentives which are balanced against the incentives of its market price. Central banks, through various schemes and machinations, eventually coopted the market for gold and developed an economic system that could create money without skin in the game; allowing them to privatize seigniorage profits and socialize any losses they incurred through inflation. Unless consequential decisions are made by people who are exposed to the results of their decisions, the system is vulnerable to total collapse; the frequent faltering of fiat currencies attests to the unfavorable asymmetry of this model for citizens.

Most commonly, as they have a direct financial incentive to do so, and with no downside to consider, central banks increase the supply of loanable funds and decrease the interest rate below its natural levels, thereby inducing an expansion of the money supply. Importantly, money supply expansion does not create any new wealth, as “printing money” does not infuse an economy with any new productive factors such as tools, factories, equipment, or human time. Instead, expansionary monetary policy only redistributes claims on productive assets from their rightful owners to those who receive the newly printed money first — usually bankers, politicians, and the other politically-favored-few closest to the spigot of liquidity (due to the Cantillon Effect). As Charles Holt Carroll said:

“Inflation is the surest way to fertilize the rich man’s field with the sweat of the poor man’s brow.”

Inflation of the money supply is a violation of private property rights, as it reallocates wealth away from its original owners (the many) into the hands of those closest to the governors of the monetary system (the few). But confiscation of wealth, via the shadow tax of inflation, is not the only collateral damage inflicted by money supply expansion. Entrepreneurs operating in these soft money economies are easily misled by the distorted price signals that centrally planned fiat currency markets inevitably cause.

To understand this, let’s look at the world through the lens of Larry the lemon farmer: emboldened by the “cheap” loans proffered by his local banker, Larry decides to borrow money to expand his lemon farm. He figures that borrowing enough money at 3% will allow him to expand and increase output of his farm by 2.5X, while only increasing his cost structure (including the 3% loan interest payable to his banker each year) by 2.3X. This economy of scale (the positive 0.2X margin between revenue growth of 2.5X and cost increase of 2.3X), Larry calculates, will drop straight to his bottom-line profit. So, Larry visits his local banker to sign the loan documents and sets out to expand his operation. At first, everything seems to be going smoothly as Larry gradually begins buying the additional land, fertilizer, and equipment necessary to grow and sell more lemons. However, things get sideways when other lemon farmers, lured by similar prospects of economic gain, also borrow from their local bank to expand their farms. As more lemon producers borrow and bid for the same lemon-farming assets, inflation sets in and prices begin to rise, thus increasing the cost structure of lemon production. Shortly after investing all his loan capital into his farm expansion, Larry finds that his cost structure has actually increased 2.8X due to more dollars chasing the same amount of productive factors for lemon farming. Gradually, then suddenly, the money Larry borrowed to expand his profit margin begins to work against him, as his increased capacity has eaten up his original profits and is now generating a loss (the negative 0.3X margin between revenue growth of 2.5X and cost increase of 2.8X, net of any prior profit margin). At this point, Larry has no choice except to increase his prices, cut costs, refinance, sell the farm, or declare bankruptcy. Under the same circumstances, other projects in other industries, misled into overborrowing by artificially cheap money, begin suffering losses as well.

An economy-wide simultaneous failure of overleveraged projects like Larry’s is called a recession. The boom and bust business cycle we have all grown accustomed to in the modern economy is an inevitable consequence of this centrally planned manipulation in the market for money. It is substantively no different than the shortages that would result if the price of bread was fixed at an artificially low level (which caused the starvation of millions in Soviet Russia). Artificially low interest rates don’t provide any benefit to the real economy, rather they simply disseminate distorted price signals that encourage entrepreneurs to embark on projects that cannot be profitably executed due to the (hard to foresee) impact of inflation on their cost structures. As with all well-functioning markets, the price of money must emerge through, and constantly reorient itself against, the natural interactions of supply and demand. Attempts to centrally plan this market only distort truth (price signals) and trigger overborrowing, recessions, and cause (or, at least, exacerbate) the boom-and-bust business cycle.

As money supplies become more opaque, so too do the critical price signals they carry back and forth between the minds of entrepreneurs.

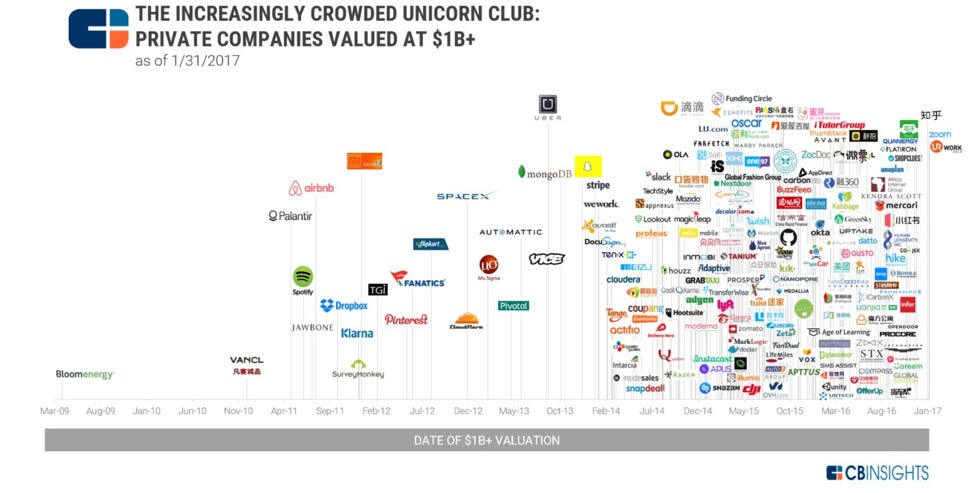

The more opaque the present and future supplies of money, the more entrepreneurs suffer from this myopia, and the more stifled the economization of human action becomes. Price signal distortions like those faced by Larry result entirely from the opacity of central bank “managed” (read: manipulated) money supplies. Central banks are only able to perpetrate this scheme due to the legal monopolies (artificial barriers against free market competition) which shield their inferior monetary technologies (fiat currencies) from facing off with superior technologies (like gold) in the marketplace. Legal monopoly protections inhibit price discovery in the market for money (the natural interest rate). There is also ample evidence that central banks actively suppress the price of gold to preserve fiat currencies (see Gata.org). Further, if monetary technologies were freely selected and priced in the marketplace, as was the case when gold ascended to dominance, then everyone could more reliably use money as a store of value instead of being forced further out along the risk curve into stocks, real estate, and other scarce assets to protect their wealth from the ravages of inflation, which further distorts prices; the increasingly crowded unicorn club reflects just how distorted prices have become:

Simply put, price is truth; distorted money supplies distort the truthfulness of price signals and throw entrepreneurial action into disarray. At the heart of the cyclic booms and busts in the economy, then, is this distortion of the fundamental signaling which, in its current distorted state, misguides entrepreneurial action. Under these conditions of monetary socialism, trying to build a business is like trying to build a house in a jurisdiction that constantly changes the spatial values of its metric system; as Taleb puts it:

According to Wittgenstein’s ruler: Unless you have confidence in the ruler’s reliability, if you use a ruler to measure a table you may also be using the table to measure the ruler. The less you trust the ruler’s reliability, the more information you are getting about the ruler and the less about the table.

With an absolutely fixed supply, Bitcoin will restore the clarity of these economic nerve signals that are so critical to proper capital allocation, risk assessment, and entrepreneurial planning. Universal units of measurement are critical in economics and industry — the seconds, meters, kilograms, and other units of measurement we use throughout the world are all immutable in value. Upon these foundations of standardized measurement, the machinery of global commerce is constructed: builders of skyscrapers, electronics, and myriad other goods rely on the constancy of these measurement units when sourcing components and materials from around the globe. Money, too, is most communicative when its supply is immutable. As a purely objective monetary medium, once it accretes enough value to incentivize its users to spend it, Bitcoin denominated price signals will carry more truth than any other money in history.

Bitcoin is a monetary channel free from the noise of unexpected supply fluctuations, which necessarily means it carries the clearest signals. In this way, Bitcoin is the perfect conveyor of the data packets on value and scarcity known as price signals.

In terms of the idea meritocracy equation, we see that fiat currency is antithetical to radical truth and, its free market corollary, truthful price signals. On the other hand, Bitcoin is the most honest money imaginable, as every component of it, including its money supply, is viewable by everyone. In a world filled with fake news, click bait, and data breaches — Bitcoin is one of the rare instances of honesty in modernity. Central banking is the reverse; it is shrouded in complexities intended to hide its truth. Bitcoin is both radically truthful and transparent.

If money is economic water, then fiat currency is inscrutably murky, and Bitcoin is crystal clear.

Bitcoin’s transparency has already shed much light on the umbral industry of central banking and its shadowy tactics by sparking a renewed interest in Austrian economics and making an entire generation ask the question: “What is Money?”. We stand to gain even more clarity around Bitcoin’s impact on the world by diving into the second element of Ray’s idea meritocracy — radical transparency.

Radical Transparency

(p.308)“By radical transparency, I mean giving most everyone the ability to see most everything.”

Originally, capitalism was founded on the cornerstones of reliably consistent rule of law, private property rights, and hard money. Respectively, these cornerstones provided people non-violent dispute resolution, confiscation resistant assets, and a sound medium of exchange. With strong and reliable rules, entrepreneurs are then free to “play the game”, accumulating capital for themselves and diffusing any innovations gleaned in the process into the whole of society. For entrepreneurs to execute effectively, they must know the rules of the game, and must be able to trust that they are not subject to change. Imagine a poker player sitting at a table where the hand-rankings changed at the whims of the casino every few hands; without sound rules on which build a strategy, no player would remain engaged for long, and would quickly exit the game. Stability in these areas is among the primary reasons why the United States is such an attractive environment for investing; for the most part, its courts function well and contract law is enforced without bias. The exception, of course, is the violation of private property rights which results from centrally manipulated money supplies — in other words, the softness of the US dollar.

According to you Ray, “The most painful lesson that was repeatedly hammered home is that you can never be sure of anything: There are always risks out there that can hurt you badly, even in the seemingly safest bets, so it’s always best to assume you’re missing something”. Considered by many to be among the safest bets in the world today is the US Dollar — it is issued by the largest economy in the world, is “backed” by the world’s most militant taxing authority, and is accepted almost everywhere as a medium of exchange. Further, by unilateral decree (and a veiled threat of force), the US Dollar exclusively denominates the lifeblood commodity of the modern industrial economy, oil. The problem with the perceived safety of the US Dollar is the opacity of the rules which govern its existence: How many are there in existence? How many will be issued in years to come? Who gets to decide? Who stands to profit from its production? Even though the US Dollar today is just an SQL database maintained by The Fed that could choose to open its records to audit, it refuses.

Instead, The Fed sets monetary policy in closed door meetings and (only vaguely) communicates its intentions using ambivalent speech. To counterbalance this opacity, an army of macroeconomists, analyst, and market commentators pour over every detail of the statements issued by central bankers including not only their words, but their tone, delivery, and even wardrobes.

Imagine a semi-governmental agency being put in charge of setting the price of, say, automobiles based on undisclosed criteria and deciding in closed-door meetings. Ask any “free market capitalist” if this seems like a good idea and he will spew vitriol at you for even suggesting such a socialistic method of managing the production of automobiles. Then ask him whether it’s a good idea for this same agency to control the price of communications technologies like laptops and smart phones. You’ll be met with the same answer and (perhaps) a loud American battle cry in support of free market capitalism. Finally, very smoothly point out to him that The Fed sets the pricing of the US Dollar (the interest rate), which is the United States’ most valuable export market, and does so based on undisclosed criteria and closed-door discussions. Although Keynesians have done a great job convincing many of the enigmatic nature of money, it is quite simply just a tool for moving value across spacetime, and as such should be priced and technologically selected on the free market (just like everything else in a truly capitalist society).

Sunlight is the best disinfectant; when everyone can see the criteria and process behind a decision they are more likely to deem in trustworthy. With Bitcoin, the algorithm which sets its monetary policy is totally transparent, meaning people can universally agree that the system is fair and unbiased. As an open-source monetary protocol, Bitcoin is essentially the principle of radical transparency in perpetual action. Similar to some of the management tools you’ve created Ray — such as the baseball cards, Dot Collector, Pain Button, etc. — Bitcoin can be thought of as a global monetary policy management tool. As a machine componentized by open-source software and entrepreneurial self-interest, it does the work facilitated by central banks today — maintaining monetary policy, reaching consensus as to account balances, and facilitating international value flows — without relying on the whims of bureaucrats who control state-backed monopolies on money. Bitcoin is the purely transparent alternative to the opacity of central banking; it is a beacon of light outcompeting an industry purposefully shrouded in darkness. Once properly understood, Bitcoin’s superior visibility inescapably enhances its believability. And once you see it, it cannot be unseen.

Bitcoin’s monetary policy (its new supply flow schedule) is becoming the most trusted in the world as it is fully transparent and unchangeable. Bitcoin runs countervailing to government monetary policy which is uncertain, opaque, and subject to change based on bureaucratic whim.

In terms of the idea meritocracy equation, Bitcoin restores the confiscation-resistance of money, which provides its users stronger property rights when compared to fiat currency. Importantly, Bitcoin also reestablishes the sorely lacking 3rd cornerstone of capitalism in an otherwise free world — hard money. As an economic good undergoing monetization on the free market, with a supply inelasticity destined to surpass that of gold, Bitcoin is resurrecting the free market capitalist triad. As it bears repeating: Bitcoin is both radically truthful and transparent.

As you’ve said Ray: (p.327) “Having nothing to hide relieves stress and builds trust.” Transparency and reliability is the essence of Bitcoin’s monetary policy. It is truly unique in that its supply is absolutely predictable and absolutely scarce. Bitcoin is the most credible monetary policy in history outcompeting the least trustworthy monetary policies in history; it is rapidly gaining a track-record superior to central banks across all dimensions — reliability, predictability, auditability, cost-effectiveness, and resistance to censorship or manipulation — thereby further eroding the believability of central bankers, which is in shorter supply with every dollar printed.

Believability-Weighted Decision Making

(p.284) “When you’re responsible for a decision, compare the believability-weighted decision making of the crowd to what you believe.”

When it comes to money, track records matter. People’s trust tends to coalesce slowly around the most stable from an exchange ratio perspective — in other words, what best maintains or gains purchasing power across time. In this respect, gold is undoubtedly the king, as it sports a more than 5,000 year history of remaining reliably scarce and, therefore, valuable. An ounce of gold has roughly equaled the price of a fine man’s suit for the past century, whereas the same suit’s price in dollars has skyrocketed. The best performing central bank fiat currency in history in the British pound, which has only lost 99.5% of its value in its 317 year existence. When it comes to value storage, gold has a believable track record, whereas fiat currencies could only barely be less believable. The hardness or soundness of money, as one of the three cornerstones of free market capitalism, has been almost completely compromised as a result of state-enforced monopolization.

For free market capitalism to function optimally, its three cornerstones — rule of law, private property rights, and hard money — must be consistently applied across all market participants. While the rule of law and property rights are (mostly) sound in western society, centrally planned money supplies are quite the opposite. Without any reliable insight into the primary governance aspects of money (see Radical Transparency above), entrepreneurs are forced to rely on other means of protecting their wealth from theft or debasement. Simply, the implementation of fiat currency offers limited to no assurances to its users that their wealth will be protected from confiscation, censorship, inflation, or counterfeit.

Fiat currencies, when stored in banks, are subject to confiscation or payment censorship by authorities. When stored physically (say, under your mattress), fiat currencies are still subject to value dilution via inflation (the legalized version of counterfeiting). Although fiat currencies offer some physical security measures against counterfeiting (the criminalized version of inflation), this has proven to be a cat and mouse game in which counterfeiters and authorities are constantly trying to outsmart one another in the domain of currency verification technologies.

Bitcoin, on the other hand, is a purely sound money and offers robust assurances to its users. It is resistant to confiscation, as only the possessor of a private key (an alphanumeric string of data) can produce the digital signature necessary to spend it. Bitcoin transactions cannot be censored due to the peer-to-peer and open-source nature of its software architecture. Complete immunity to unforeseen changes in its money supply is guaranteed by unbreakable cryptography and the economic self-interest of miners which secure its network. Finally, since the rules which govern Bitcoin can be verified by anyone, anywhere, and at any time — it is completely counterfeit resistant. Indeed, it is its radically transparent nature that makes Bitcoin the most believable monetary technology in history. Monetary opacity always leads to moral hazard on the part of policymakers.

With decades of experience seeing these hazards explode up close, Ray has said, (p.107) “The job of a policymaker is challenging under the best of circumstances, and it’s almost impossible during a crisis. The politics are horrendous and distortions and outright misinformation from the media make things worse.” So this begs the question: why should we permit policymakers to dictate monetary policy? As “free market capitalists”, we make no such concessions in any other market in the world. We don’t trust a board of governors to tell us how many automobiles to manufacture or at what price to sell laptops each year, so why should we trust central banks to set price and production targets in the largest market in the world? As with all production decisions, the free market — representing the collective interests, intelligence, and wisdom of all economic actors — is always the best generator of (low) believable prices, new innovations, and consumer satisfaction.

Controlling monetary policy is like being crowned king of the world. As a fat-cat banker once said:

For this reason, most of the world’s wars have been waged in an attempt gain control over this contentious crown. And to control monetary policy, it is necessary to dominate the original monetary sovereignty layer of planet Earth — gold. For instance, during World War II, North America became a geographically-strategic safe haven for European gold hoards to protect them from Nazi plundering. At the conclusion of World War II, into which the United States ultimately intervened to destroy its war-wearied opponents and declare itself victorious, the Brettonwoods Conference was convened in which the rules of the global economic order were rewritten by the newly self-proclaimed king — the United States. This conference cemented The Fed as the effective central bank of the world and the US dollar as the world reserve currency.

Even if you are a believer in monetary socialism, you would be hard pressed to defend the believability of central bankers. As you said Ray, “Think about people’s believability, which is a function of their capabilities and their willingness to say what they think. Keep their track records in mind.” In terms of capabilities, central banks have arrogated themselves virtually unlimited latitude to manipulate the supply and price of fiat currency. However, they have exercised these privileges based on (largely) undisclosed criteria and are notorious for their veiled communication styles. In other words, central bankers seem quite unwilling to say what they think (which violates the first thing necessary for an idea meritocracy) and their decision-making criteria are shrouded in falsehood. As Michel de Montaigne once wrote:

“If falsehood had, like truth, but one face only, we should be upon better terms; for we should then take for certain the contrary to what the liar says: but the reverse of truth has a hundred thousand forms, and a field indefinite, without bound or limit.”

In regards to track records, central bankers likely hold the world record for the most abysmal performance history. Since reputation cannot be printed, and must be earned through a lifetime of honesty, it is unsurprising that central banks have struggled in this respect. Historically, every fiat currency has trended towards worthlessness, which has only dragged the believability of this monetary model ever-downward. Mandated with price stabilization and employment maximization, The Fed has failed miserably at both, especially since severing the peg to gold in 1971; here, we show the US dollar’s loss of purchasing power since 1775:

Central banker opinion-driven money supplies are proportionately reliable to the value storage functionalities of the ever-softening fiat currencies they mass produce. Bitcoin’s fact-driven money supply is as reliable as the mathematics and thermodynamics which sanctify its inviolable ledger. Opinions are like soft money, in that they can easily be diluted and distorted. Facts are like hard money, in that they are rooted in scientific realities. Said simply: do we believe the largest market in the world is best governed by opinion or fact? Buying Bitcoin is buying a put option on central banker malfeasance. As Travis Kling says:

More fundamentally: how can we possibly believe that central bankers will perform well when they completely lack skin in the game? As Taleb puts it:

“Systems don’t learn because people learn individually –that’s the myth of modernity. Systems learn at the collective level by the mechanism of selection: by eliminating those elements that reduce the fitness of the whole, provided these have skin in the game. Food in New York improves from bankruptcy to bankruptcy, rather than the chefs individual learning curves –compare the food quality in mortal restaurants to that in an immortal governmental cafeteria. And in the absence of the filtering of skin in the game, the mechanisms of evolution fail: if someone else dies in your stead, the build up of asymmetric risks and misfitness will cause the system to eventually blow-up.”

Totally disconnected from the consequences of their policy actions, which are instead born by citizens, central bankers are incentivized to maintain the status quo to preserve their jobs and “prestige”. Money, the largest and most critical market in the world, simply cannot evolve without practitioners who are subjected to real world consequences and tradeoffs, in real time. Simply, if you lack skin in the game then you lack believability. This explains why ancient Roman architects were required by law to stand beneath their monolithic arches when the scaffolding was removed. This (deadly) disincentive to malperformance worked wonders, as some of the oldest arches constructed in this way are still standing at over 2,000 years of age. If only central bankers were subjected to the devastation they inflict on centrally planned economies should their decision-making not work out, then perhaps the world would still be on a gold standard and the dire need for Bitcoin would be lessened.

Parading themselves as the healers of economic crises, central bankers are actually the creators of these calamities. QE, TARP, NIRP, and other interventions inflict a heavy iatrogenic cost on society; and the harm done is further compounded by the agency problem (central bankers have no skin in the game, and therefore have conflicted interests when it comes to managing money supplies).

So, in terms of the idea meritocracy formula, it is clear that central banking fails to satisfy its third element of Believability-Weighted Decision Making, instead, the prevailing economic order seems to promote the least believable people into the driver’s seat of the world economy. Translated into the free market formula terms, this is an expectant result as these policymakers suffer from the agency problem and are rendered impotent without “Skin in the Game”-Weighted Decision Making. In this sense, Bitcoin is the reverse; its node operators and miners govern the system, all of whom have skin in the game and, therefore, possess more believable decision-making capabilities — just like the ancient architects who stood beneath their newly un-scaffolded arches.

To put it all together in terms of our original equations; we began with:

“Idea Meritocracy = Radical Truth + Radical Transparency + Believability-Weighted Decision Making”

Which translates to this free market format:

Free Markets = Truthful Price Signals + Transparent and Reliable Rule of Law, Private Property Rights, and Hard Money + “Skin in the Game”-Weighted Decision Making

Based on what we’ve learned so far, we can translate these equations once again into central banking and Bitcoin versions:

Central Banking = Untruthful Price Signals + Transparent and Reliable Rule of Law, Marginalized Private Property Rights (due to violations via inflation), and Soft Money + “Agency Problem”-Weighted Decision Making

Bitcoin = (Absolutely) Truthful Price Signals + Transparent and Reliable Rule of Law, Private Property Rights, and (Absolutely) Hard Money + “Skin in the Game”-Weighted Decision Making

Clearly, only Bitcoin is 100% consistent with the equation for free markets; whereas fiat currency is almost entirely inconsistent. Since this free market equation is equivalent to the idea-meritocratic equation, we may deduce: Bitcoin is completely consistent with Ray’s formulation of the idea meritocracy, and fiat currency is not.

Therefore, because math, Bitcoin is both a free market and an idea meritocracy.

So, Ray, assuming your Principles are stated forthrightly, how can you possibly be a non-believer in Bitcoin? As you said Ray, (p.379) “When someone says ‘I believe X,’ ask them: What data are you looking at? What reasoning are you using to draw your conclusion?” So let me ask you Ray: after Bitcoin’s impeccable performance for over a decade (over 99.98% uptime, never been hacked, evolution into the most secure computing network in the world, roughly $200B in market capitalization, and over $1T of transactions cleared in total), what data and reasoning are you using to draw your conclusion about Bitcoin?

My guess is that like many smart people, you may have disregarded Bitcoin at the outset. In accordance with one of your favorite principles, I implore you to keep an open mind about Bitcoin and, perhaps, you will come to see it as an embodiment of open-mindedness itself. In that spirit, let’s dive deeper.

In Part 4, we will continue our exploration of Ray’s principles and their relationship to Bitcoin/money, beginning with open-mindedness.