An Open Letter to Ray Dalio re: Bitcoin (Part 5)

An Open Letter to Ray Dalio re: Bitcoin (Part 5)

An open letter to hedge fund colossus Ray Dalio regarding his worldview, the forces of financial nature, and how Bitcoin is bound to reshape both.

Part 4 went through Ray’s principles of open-mindedness, faith in nature, and chains of cause and effect. In Part 5, we continue our exploration of Bitcoin and money through the lens of Ray’s principles, beginning with evolution.

Evolution

(p.142) “Evolution is the single greatest force in the universe; it is the only thing that is permanent and it drives everything.”

Change is the only thing that never changes. And when something is finished changing, it is finished. As such, all things exist in either a state of evolution or devolution:

Whether improving or declining, all things exist in flux. As you’ve said Ray, (p.142) “As I thought about evolution, I realized that it exists in other forms than life and is carried out through other transmission mechanisms than DNA. Technologies, languages, and everything else evolves.” Money, like a spoken language, is an informational protocol. Unlike language, money has evolved to inhabit many different forms. Seashells, salt, cattle, beads, stones, precious metals and government paper have all functioned as money at one or more points in history. Even today, forms of money still spontaneously emerge with things like prepaid mobile phone minutes in Africa or cigarettes in prisons being used as localized currencies. Different monetary technologies are in constant competition, like animals competing within an ecosystem. Although instead of competing for food and mates like animals, monetary goods compete for the belief and trust of people.

Historically, the hardest monetary technology to produce which exhibits otherwise comparable monetary traits (durability, divisibility, portability, recognizability) outcompetes more easily produced forms to become dominant on the free market — an asset that succeeds in this way is called hard money; a technology that is discovered through market-driven natural selection.

As we have learned, the rise of fiat currency was the result of governments coopting gold — which had risen to global dominance on the free market because of its superior scarcity relative to other monetary metals, which themselves exhibited superior monetary characteristics compared to other monetary technologies (like seashells, salt, cattle, etc.). By issuing paper money redeemable in gold, governments were able to resolve its one drawback — suboptimal divisibility. However, governments eventually eliminated redeemability of paper money for gold, thus ushering in the age of fiat currency. Lack of scarcity would have resulted in the extinction of fiat currency long ago if it weren’t for the anticompetitive efforts of governments in the gold markets (if you haven’t yet, check out Gata.org). In this sense, gold is the last freely chosen money in the marketplace and fiat currency is but an apparition of this multi-millennia-old monetary metal; a deception that has been haunting human progress since its inception in 1971. As Taleb describes it:

“…institutions block evolution with bailouts and statism. Note that, in the long term, social and economic evolution nastily takes place by surprises, discontinuities, and jumps.”

In free markets, competition generates the information that vitalizes innovation — the man-made type of evolution. Completely isolated from the discipline of the market by legal monopoly, central bank issued fiat currencies have softened tremendously, in both value and functionality. This is unsurprising: any complex system — whether it be a technology, an economy, or an organism — that is isolated from the shaping of competitive forces will naturally devolve over time. As you’ve observed Ray, (p. 147) “One of the great marvels of nature is how the whole system, which is full of individual organisms acting in their own self-interest and without understanding or guiding what’s going on, can create a beautifully operating and evolving whole. While I’m not an expert at this, it seems that it’s because evolution has produced a) incentives and interactions that lead to individuals pursuing their own interest and resulting in the advancement of the whole, b) the natural selection process, and c) rapid experimentation and adaptation.” This marvelous dynamic is at the heart of free market competition, open-source adaptation, and Bitcoin which, as we have seen, is both a free market in and unto itself and an open-source instance of digital hard money.

Bitcoin is an evolutionary leap forward for money: it combines the divisibility, durability, portability, and recognizability of pure information with the absolute scarcity of time to form the most impeccable monetary technology the world has ever known.

As you’ve said in regards to evolution, (p. 124) “I realized that passing on knowledge is like passing on DNA — it is more important than the individual, because it lives way beyond the individual’s life.” Ray, isn’t it time for humanity to transition to a form of money that exists beyond the schemes, machinations, and manipulations of those who are able to wrest control of its governing mechanisms? By centering an evolved monetary social contract on an immutable ruleset, we can eliminate the incentives to fight over gold or international reserve currency status and therefore enhance mankind’s cooperative capacity, which in turn will accentuate the division of labor, enhance productivity, and increase aggregate wealth creation worldwide. It’s time for money to be governed by rules instead of rulers, and Bitcoin gives us the opportunity to make this transition once and for all. Imagine how much human ingenuity could be freed up worldwide if we eliminated the need for monetary policymakers, the army of analysts who watch them under a microscope, and the heavily distorted price signals caused by soft money.

Each of us are nodes of information — biological machines expressing our genetics, experiences, and ideas — that are collectively best served by successfully minimizing impediments to expression like policies, hierarchies, and illegitimate institutions. As Noam Chomsky said:

“Institutional structures are legitimate insofar as they enhance the opportunity to freely inquire and create, out of inner need; otherwise, they are not.”

Modes of organization which favor merit-based competition and rely on natural selection to determine which ideas flourish help us flourish. This is the free market (and idea meritocratic) paradigm: unobstructed exchange is always superior to that which is centrally intermediated, regulated, or manipulated. Dissimilar to cognitive learning, evolution does not distinguish between the observer and the observed, enabling it to “learn at the edges” by absorbing the successes and failures of its constituents (cells, individuals, exchanges, or businesses) through a filter of natural selection and incorporating them into its own form (a body, society, market, or economy).

Global free markets, coordinated via truthful price signals, can be thought of as a human hive-mind constituted of innumerable interpersonal exchanges; an organic, bottom-up system in which resources, risks, and human time are priced and allocated according to the prevailing economic realities faced by society. This collective mind is the macrocosm of our individual mind microcosms, which have naturally evolved in a bottom-up way. Existing as illegitimate, closed-source economic fiefdoms, central bank money monopolies inhibit natural selection and diminish the evolutionary potential of our global collective mind.

As you’ve observed Ray, (p.213) “This universal brain has evolved from the bottom up, meaning that its lower parts are evolutionarily the oldest and top parts are the newest.” Why should we expect the amalgamation of human economic actions to evolve any differently? Free markets enable price and technology discovery from the bottom up, as they completely lack any centralized governing body. Hard money has always evolved on the free market and is the norm of human history; only over the past century has it been so explicitly coopted by a few at the expense of everyone else.

Using a Darwinian analogy: what natural selection is to gold, artificial selection is to fiat currency. In the same way mankind created designer dogs from wolves, or Monsanto self-terminating seeds from naturally-occurring seeds, so did he create fiat currency from gold. Bitcoin, as an unstoppable free market money being naturally selected for favorably in the marketplace, may in this sense be considered the reemergence of hard money in the modern world; a natural reversion to the free market foundations of money through an evolved (and evolving) monetary technology.

As a hard money that is monetizing in real time, Bitcoin outcompetes other forms of money in market-driven natural selection, whereas fiat currencies exist exclusively due to monopoly-driven artificial selection. As Bitcoin transcends the artifices that preserve the monopolistic position of fiat currencies, it forces these monetary technologies to compete based on their own (inferior) merits, and promises to push them into extinction.

One would be hard pressed to find a worse technology from both a functional and societal value-add standpoint. As you’ve said Ray, (p.272) “To be good, something must operate consistently with the laws of reality and contribute to the evolution of the whole; that is what is most rewarded.” In this sense, fiat currencies are bad — really bad. Not only do they give politicians a lever by which to control people, they also erode societal cohesion as their primary function — the storage of value across time — is repeatedly compromised in favor of multifarious political agendas all over the world. As Taleb says:

“…it is downright irrational if one holds onto an old technology that is not naturalistic at all yet visibly harmful, or when the switch to a new technology… is obviously free of possible side effects that did not exist with the previous one. And resisting removal is downright incompetent and criminal (as I keep saying, the removal of something non-natural does not carry long-term side effects; it is typically iatrogenics free).”

Viewed on a grander scale, Bitcoin seems to be a natural evolutionary step towards freer society:

· Gutenberg’s Printing Press gave us decentralized analog knowledge (which separated Church and State)

· Democracy gave us decentralized government

· The internet gave us decentralized digital knowledge

· Bitcoin gave us decentralized digital money (which may one day separate Money and State)

Indeed, it is amazing that a lone, anonymous programmer released an open-source protocol that is now a viable contender for the world reserve currency whereas Facebook, one of the most flush corporations in the world, has been unable to move forward with its currency project due to regulatory roadblocks. Digital technology reshapes reality, and decentralization enables us to create leaderless organizational structures based more so on rules than rulers. Bitcoin is the latest and greatest expression of this overarching trend away from centrality and towards a more natural ordering of things.

Like you Ray, I consider myself a shaper who experiences “the gap between what is and what could be as both a tragedy and a source of unending motivation.” I see a world shackled in financial slavery, with central bankers and their inner circles as the great parasites of wealth created by working people all over the world. Centrally planned money is straight out of the socialist playbook and, aside from a brief period in the late 19th century when the world was mostly on a gold standard, we have never seen a truly free market for money. An economy is like life itself; in life, we do not expect to understand events as they occur, at least with total causality and clarity in mind, but looking back on them we gain a better understanding. Bitcoin is alive; while it is impossible to say where it is heading with certainty, it is monetizing and evolving in real time, and its proponents all have skin in the game.

Evolution can only happen if the risk of extinction is present. Only systems with skin in the game are capable of evolution; absent this, devolution becomes inevitable. Systems learn and evolve through the death of their components; the biological manifestation of this via negativa process is called apoptosis. Any institution that cannot glean lessons from its undying components loses touch with reality as it grows until nature ultimately overrules its energetic imbalance in a mighty swing of the universal pendulum — whether by way of renaissance or revolution.

Therefore, we evolve best by sharpening our organizing principles against the palpable feedback gathered from falsifiable entrepreneurial experiments conducted at the front lines of our understanding, where each failure edifies the economic ensemble as to what does not work so that its next individual efforts will be emboldened by the greater experience gained. In this way, we are better served by the free market, with its bricolage of tactile sensory inputs from its entrepreneur-led, optionality-rich explorations of economic realities instead of the unwavering unidirectionality of a centralized plan. The choice of the technology we use as money is best arrived at in an uninhibited marketplace in the same way other technologies are invented, shaped by competitive forces, and tinkered with over time; in accordance with the timeless principle behind both innovation and evolution.

Timelessness

(p.121) “With time and experience, I came to see each encounter as “another one of those” that I could approach more calmly and analytically, like a biologist might approach an encounter with a threatening creature in the jungle: first identifying its species and then, drawing on his prior knowledge about its expected behaviors, reacting appropriately.”

History doesn’t repeat, but it does rhyme. Every moment and person are unique, but they tend to conform to some prior pattern or archetype. Personality types can be characterized and filtered by a variety of metrics including Meyers-Briggs and management tools like the Baseball Cards Bridgewater uses. Modern-day events are often foreshadowed by historical happenings. By thoughtfully studying these archetypal forms of characters and events, we are better equipped to deal with the uncertainties inherent to life and work. As the axiom says, “Those who do not learn history are doomed to repeat it.”

Bitcoin is often called digital gold for a good reason; the best analogy for its emergence is the monetization of gold. Money is a market pricing and coordination mechanism for human time; it reflects the present value of the (liquid) time savings generated by subdivided labor and denominates prices. The relative inelasticity of gold’s supply to other monetary metals is the reason it outcompeted them to become dominant in the free market before central banking commandeered it (seriously, check out Gata.org). Its ascent as money is based on timeless economic principles from the Austrian school. Despite the justifications for schemes like fiat currency in 1971 (revoking dollar redeemability for gold was said to be a “temporary” measure) and MMT today, the minds of prominent historical figures agreed universally that only monetary metals were actual money:

- JP Morgan said in his 1912 testimony to congress: “Money is gold, and nothing else.”

- Thomas Jefferson is quoted as saying: “Paper is poverty, it is only the ghost of money, and not the money itself.”

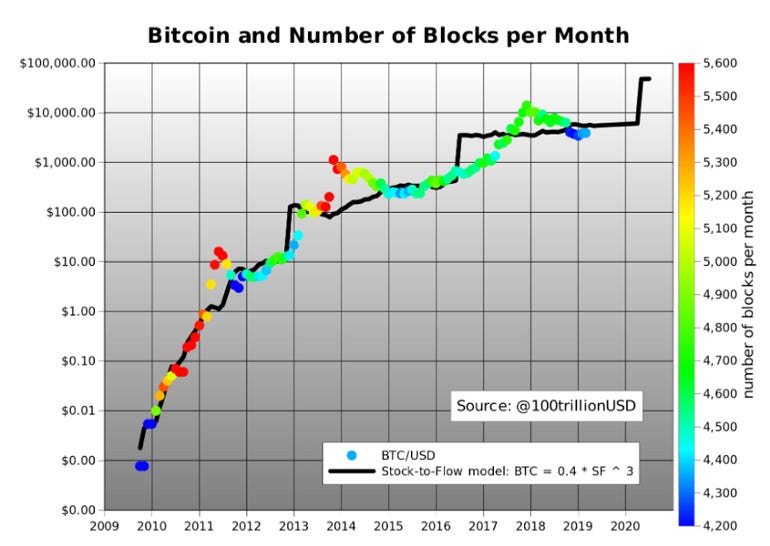

Even you Ray once said: “If you don’t own gold, you know neither history nor economics.” In the free market, fiat currency has never existed. Only through state intervention has money come under monopoly control; the state had no more of a hand in the development of money than it did language. So, to understand the ascent of Bitcoin from a quantitative perspective, we must first understand how gold came to dominate the market for money. In his masterful work The Bitcoin Standard, Saifedean Ammous sheds light on how Bitcoin can be perceived as “another one of those” in the sense that it is following a similar monetization path as that followed by gold. In short, throughout history societies have naturally coalesced around the monetary technology exhibiting the highest “stock-to-flow” ratio. When we look at the stock-to-flow quantitative model put together by PlanB, we see that the Bitcoin price has an extremely high correlation to this key valuation metric:

Said simply, the attribute of money that causes it to retain its value is its scarcity. As a former commodities trader Ray, I am sure you will understand the value of this model. In free market monetary competition, the scarcest money wins, as it is superior at protecting wealth across time. Bitcoin is on an inevitable path to become the highest stock-to-flow asset in human history, overtaking gold by a factor of two in the year 2024. Bitcoin’s ever-constricting new supply flow as a percentage of existing stock is encouraging its adoption first as a store of value before it begins fulfilling the other functions of money more adequately. This is consistent with the monetization path taken by gold — as the classical economist William Stanley Jevons remarked:

Historically speaking, gold seems to have served, firstly, as a commodity valuable for ornamental purposes; secondly, as stored wealth; thirdly, as a medium of exchange; and, lastly, as a measure of value.

So, in terms of monetization, Bitcoin is “another gold” following a similar evolutionary path — collectible, store of value, medium of exchange, and finally a unit of account. In an even deeper sense, Bitcoin can be considered “another one of those” as a part of the resurgence of ancient wisdom in the modern world. Yoga, meditation, Ayurvedic medicine, mindfulness, paleo diets, Ayahuasca, acupuncture — citizens of the digital age are rediscovering the deep roots of humanity. As the collective learnings of mankind are now accessible to everyone with an internet connection, this is likely a key driver of this worldwide phenomenon. Bitcoin, as a pure expression of Austrian economic thought, is yet another case of ancient wisdom’s resurgence into modernity. By releasing the economic juggernaut that is Bitcoin into a world dominated by monopoly money, Satoshi put Keynesian economics and its “highly mathematized” theories (central bank circumlocutory propaganda) to the test and, thus far, has succeeded wildly in disproving their validity.

Bitcoin is the best performing asset in human history, even when its sharp drawdowns are taken into account. It has offered the highest risk-adjusted rate of return of any asset class over the past decade (as quantified by the Sharpe ratio), and outperforms even further when only the negative volatility is taken into account (most of Bitcoin’s price volatility has been positive). Indeed, it has been difficult to invest in Bitcoin unsuccessfully:

As you’ve said Ray, “the greatest success you can have as the person in charge is to orchestrate others to do things well without you.” This is exactly what Bitcoin does for all current and future generations; it takes monetary policy out of the sphere of political influence and protects it with timeless, immutable, and mathematically-enforced rules beyond the machinations of mankind. These rules are fixed and fully transparent — resistance to confiscation, censorship, inflation, and counterfeiting — for all to see and rely upon across time. In this sense, Bitcoin is a timeless monetary system into which people can escape the walled-garden economies of a central bank dominated world; an man-made antidote to the poisoned society of man — as Henry Miller described it:

“Society had so complicated the relations between men, had so enmeshed the individual with laws and creeds, with totems and taboos, that man had become something unnatural, something apart from nature, a phenomenon which nature herself had created, but which she no longer controlled.”

By providing a more sound substrate for economic planning and coordination, Bitcoin promises to reduce the toxic bureaucracies that have festered around the central banking model. Outfitted with a sound store of value, people will no longer be forced out further along the risk curve to protect their wealth, making real estate more affordable and unicorn companies more rare. As state revenues naturally decline as a result, government-sponsored “zombie” companies and monolithic “too big to fail” institutions will gradually slip into irrelevance. Finally able to protect their wealth from confiscation via inflation, people will be better equipped to capitalize their own businesses and pursue their dreams. And a world in which people are doing what they love is better for everyone. The majority of most people’s lives is spent working to earn money, and Bitcoin stands to change the very nature of both work and money. In this sense, Bitcoin is bound to change mankind more than he will ever change Bitcoin.

Meaningful Work

(p.538) “We work with others to get three things: 1) Leverage to accomplish our chosen missions in bigger and better ways than we could alone 2) Quality relationships that together make for a great community 3) Money that allows us to buy what we need and want for ourselves and others… (p.216) man is perpetually suspended between the two extreme forces that create us: ‘Individual selection which prompted sin and group selection which promoted virtue.’”

Since time immemorial, man has been driven to take both selfish and selfless actions. The principles which guide people’s actions are a composite of family values, social experience, incentive structures, and natural predilection. Many of us inherit the political and religious leaning of our parents or family, which influence our value systems. However, our experience in the world also shapes (and continually reshapes) our values as well. These external influences are both, of course, undergirded by our natural inclinations and preferences. In short, we are all born unique, but are also products of our environments. Money, as the most interconnective social phenomenon in the world, is one of the most significant external forces shaping our thinking, planning, preferences, relationships, and actions. Think about it: how many times have you thought or talked about money in the past 24 hours? For most of us, many, many times. The nature of the money we use is a powerful determinant of whether we act viciously or virtuously.

In this respect, Bitcoin has an interesting impact on personal character. As Jimmy Song laid out (here, here, and here), Bitcoin (and hard money more generally) encourages people to develop virtues such as prudence, temperance, and justice. Since fiat currency suffers from perpetual dilutions of value, its users are incentivized to spend and borrow; in other words, to be less prudent with their money. Bitcoin is the reverse; its fixed supply and diminishing inflation rate ensures that it appreciates as global economic output grows and incentivizes people to save and invest. As more people adopt Bitcoin, their time preferences are shifted to become more future-oriented. In this way, Bitcoin encourages people to treat the future as something to be invested for instead of borrowed against.

Since its supply is unmanipulable, Bitcoin is gradually eroding the financial capability of governments to provide guarantees in the form of welfare or bailouts. It’s easy to see how this softens temperance: if you knew your job were guaranteed no matter your performance, how hard would you try? Similarly, a long history of tax-payer funded bailouts for failed banks without skin in the game have encouraged them to take on steadily more risk, as any gains realized from their efforts accrue to their shareholders whereas any catastrophic losses that are incurred are paid for by taxpayers (against their will). This contradicts the tradition in ancient Catalonia, in which failed bankers were beheaded in front of their banks (talk about skin in the game). By providing a means of privatizing gains and socializing losses, governments cause the market to misprice risk and erode the value of temperance: the skill of rightsizing one’s exposures in life on the risk and reward spectrum. With the risk of failure removed, beneficiaries of government guarantees no longer have skin in the game, and therefore take on risks intemperately. Repeated blow ups and taxpayer anger, as savings are eroded to bail out “too big to fail” institutions, fragilizes the delicate bonds that hold society together.

Justice is embodied in fair treatment; it encompasses integrity, honesty, and respect. When an action is taken that benefits one group disproportionally at the expense of another, we can say that it is unjust. Inflating money supplies is an unjust action, as it does not offer a single equitable benefit, and instead enriches the politically-favored few closest to the monetary spigot at the expense of the many farther away from it. Using inflation as a means of funding welfare and warfare, new government programs are continually implemented while old ones are kept functional despite their inefficiency or uselessness. As Milton Friedman once said, “Nothing is so permanent as a temporary government program”. Again, government intervention severs skin in the game and decouples the intention of these programs from their results. The impact of this is a swelling class of government dependents, workers, and contractors that function inefficiently and only exist because of the government’s ability to create new money. Interventionism of this kind distorts the information provided by market pricing and, therefore, makes fair dealings much more difficult. In a free market run on hard money, only industrious people who add value and deal fairly in an economy are rewarded. Paradoxically, as governments strive to ensure equality of outcomes, they incentivize unjust treatment. At the core of this rottenness is monetary inflation: a legally enforced injustice.

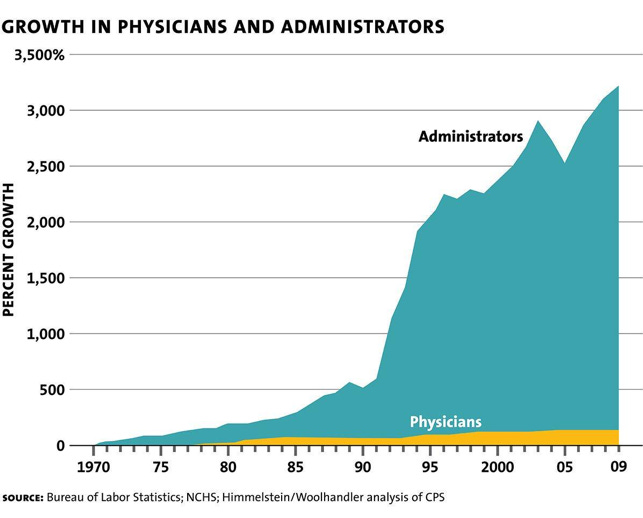

In an economy run on soft money, intermediary business models and professional roles designed to extract value from the money that originates at the center (the central bank) and flows outward into an economy (through successively lower tier banks and eventually to businesses and consumers) start popping up everywhere. These intermediary functions add little value to an economy yet capture a disproportionate share of the value of economic output; a dynamic commonly called “rent-seeking” that is unsurprisingly pervasive in industries that suffer from extensive government meddling like healthcare, education, and banking. After the last vestiges of hard money were abandoned in 1971, rent-seeking has exploded; consider the case of healthcare:

Meaningful work is being compromised by central banking. There has been a demographic shift from value-additive to value-subtractive positions — as evidenced by the training of more bankers than engineers, or the academic credentialing transition from medicine to finance. In a free market, compensation is reflective of a role’s usefulness to society. But with monetary socialism, there are greater financial incentives to work closer to the spigot of fiat currency in roles that are mostly non-productive and extractive. Hayek summed this up nicely:

“It is not merely that if we want people to give their best we must make it worthwhile for them. What is more important is that if we want to leave them the choice, if they are to be able to judge what they ought to do, they must be given some readily intelligible yardstick by which to measure the social importance of the different occupations. Even with the best will in the world it would be impossible for anyone intelligently to choose between various alternatives if the advantages they offered him stood in no relation to their usefulness to society.”

One more thing: most rent-seeking jobs suck! How many accountants, bankers, or administrators do you know that “love” their job? Many of these jobs are a direct result of the lacking social scalability inherent to monetary socialism. The more we can globally standardize onto a hard money, the more productivity we generate collectively, the lower the cost of living becomes, and the less we have to work individually.

Money is just a means to an end: as you’ve said Ray, (p. 417) “Remember that the only purpose of money is to get you what you want, so think hard about what you value and put it above money.” I think it’s safe to say that most people want to live a fun and productive life full of fulfilling relationships. To this end, the type of money society runs on is of paramount importance. The utility, supply, and value of fiat currency cannot be trusted; since money is the trust network through which all of our commercial relationships are carried out, this lack of trust in the money infects the trust relationships amongst its users. Again, to get what we want, we need reliable protocols for commercial interaction like private property rights, rule of law, and manipulation-proof money. As central banks confiscate and redistribute wealth created by the work of others, they cut these cornerstones of capitalism and weaken the foundations of civilization.

Money and speech are media of expression; any inhibition or censorship of these societal building tools, which together are responsible for nearly all human coordination and communication, contradicts the most basic liberties (1st Amendment in the US) intrinsic to Western Civilization. There is zero justification for a system that suppresses verbal or financial expression. By organizing ourselves within a truly free market capitalist system that incentivizes basic morality (don’t steal, don’t kill), we can advance our civilization to new levels and dramatically improve the quality of human relations.

In Part 6, we will continue our exploration of Ray’s principles and their relationship to Bitcoin/money, beginning with meaningful relationships.